CryptoSlate

CryptoSlate

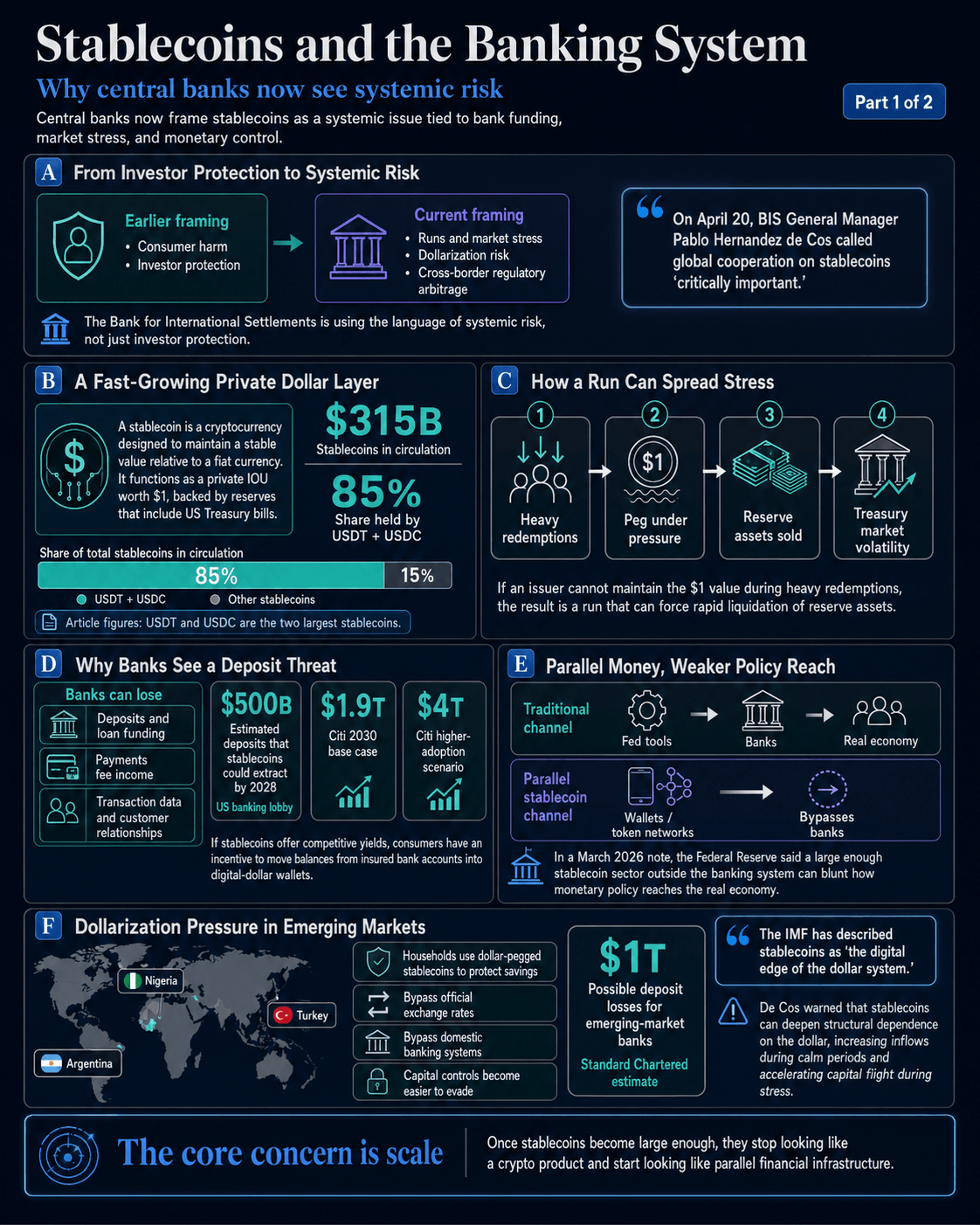

The Bank for International Settlements sharpened its stablecoin stance on April 20, with General Manager Pablo Hernandez de Cos calling global cooperation "critically important" and warning of runs that could spill into Treasury markets, dollar-pegged tokens accelerating dollarization in developing economies, and fragmented rules private firms can arbitrage across borders. It's the language of systemic risk, a step beyond the investor-protection framing that dominated earlier debates.

Tether's USDT and Circle's USDC account for roughly 85% of the $315 billion in stablecoins currently in circulation. Citi's April 2026 research projects issuance at $1.9 trillion by 2030 in its base case, with $4 trillion possible under higher-adoption scenarios, figures that are now actively shaping central-bank planning horizons.

Why it matters

The concern isn't whether the $1 peg holds. The deeper fear is what stablecoins do to the banking system as they scale: deposits migrate to private wallets, banks lose the funding base for loans, and payments settle on token rails that bypass them entirely. The ECB has modeled what $2 trillion in stablecoins would mean for European financial stability and concluded the sector becomes a direct transmission channel for American financial stress into European banks.

The US banking lobby has estimated stablecoins could extract roughly $500 billion in deposits by 2028, while Standard Chartered puts emerging-market bank deposit losses at as much as $1 trillion. The Fed's March 2026 note added a further wrinkle: a stablecoin sector large enough to live outside the banking system can blunt how monetary policy reaches the real economy, because the Fed's tools work through banks.

Market impact

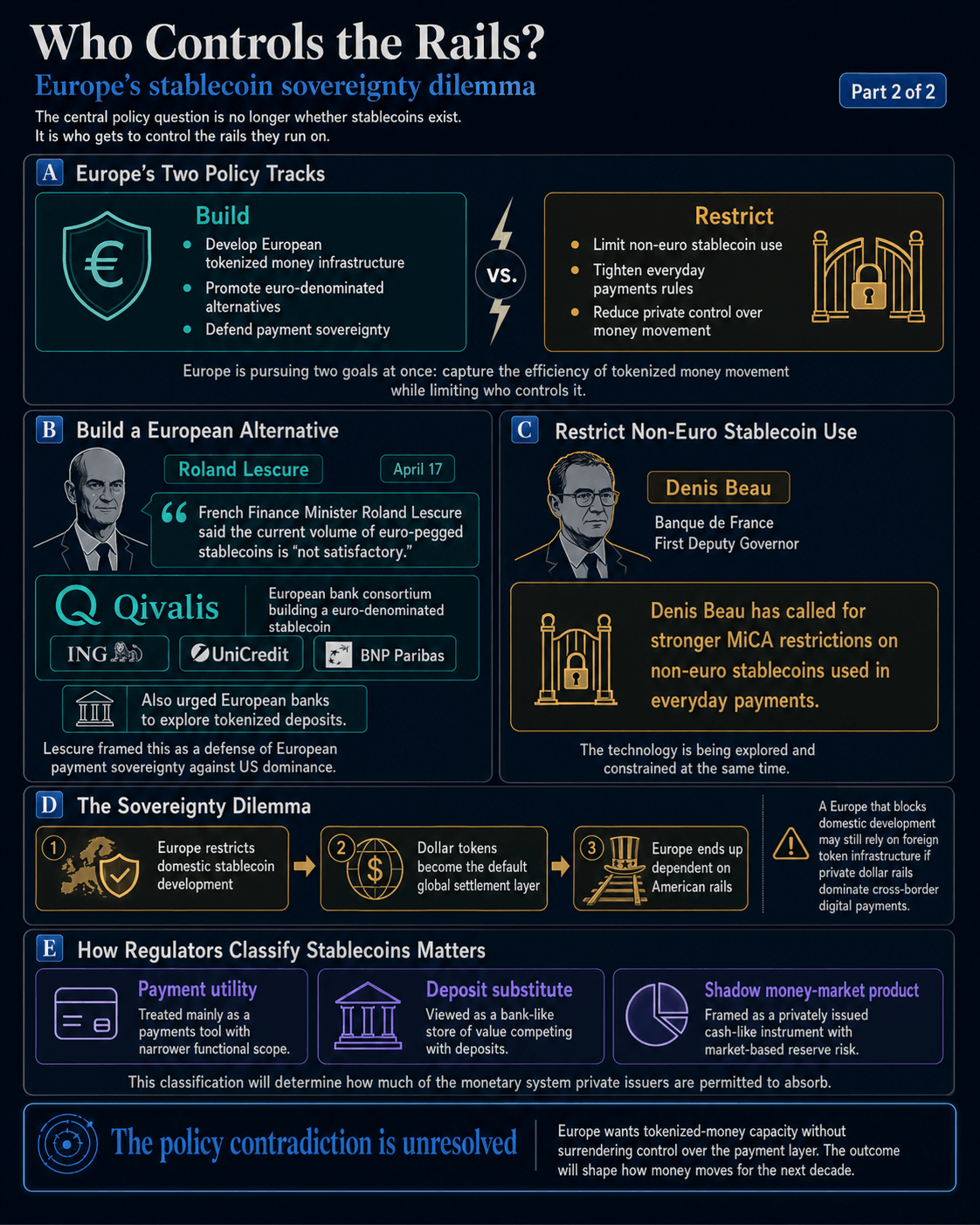

European policymakers are running two contradictory tracks at once. French Finance Minister Roland Lescure endorsed Qivalis, a euro stablecoin backed by ING, UniCredit, and BNP Paribas, calling euro-pegged volume "not satisfactory," while Banque de France First Deputy Governor Denis Beau pushes for tighter MiCA restrictions on non-euro stablecoins in everyday payments. The contradiction — wanting the efficiency of tokenized money while rejecting private control of it — is unresolved.

The IMF's framing captures the structural threat: stablecoins as the digital edge of the dollar system, extending US dominance faster and more directly than the eurodollar system ever did, through private companies rather than state institutions.

Frequently asked questions

-

What did the BIS say about stablecoins on April 20?

BIS General Manager Pablo Hernandez de Cos called global cooperation on stablecoins "critically important" and warned of runs that could trigger market stress, dollar-pegged tokens accelerating dollarization in developing economies, and fragmented regulatory frameworks private firms can arbitrage across borders.

-

How large is the stablecoin market right now?

Roughly $315 billion in stablecoins are currently in circulation, with Tether's USDT and Circle's USDC together accounting for about 85% of that total.

-

What does Citi project for stablecoin growth by 2030?

Citi's April 2026 research projects stablecoin issuance at $1.9 trillion by 2030 in its base case, with $4 trillion possible under higher-adoption scenarios.

-

How much in bank deposits could shift to stablecoins?

The US banking lobby has estimated stablecoins could extract roughly $500 billion in deposits by 2028, while Standard Chartered estimates emerging-market banks could lose as much as $1 trillion.

-

What is the policy contradiction inside Europe on stablecoins?

French Finance Minister Roland Lescure endorsed the Qivalis euro stablecoin from ING, UniCredit, and BNP Paribas, while Banque de France First Deputy Governor Denis Beau is simultaneously pushing for stronger MiCA restrictions on non-euro stablecoins used in everyday payments.