CoinDesk

CoinDesk

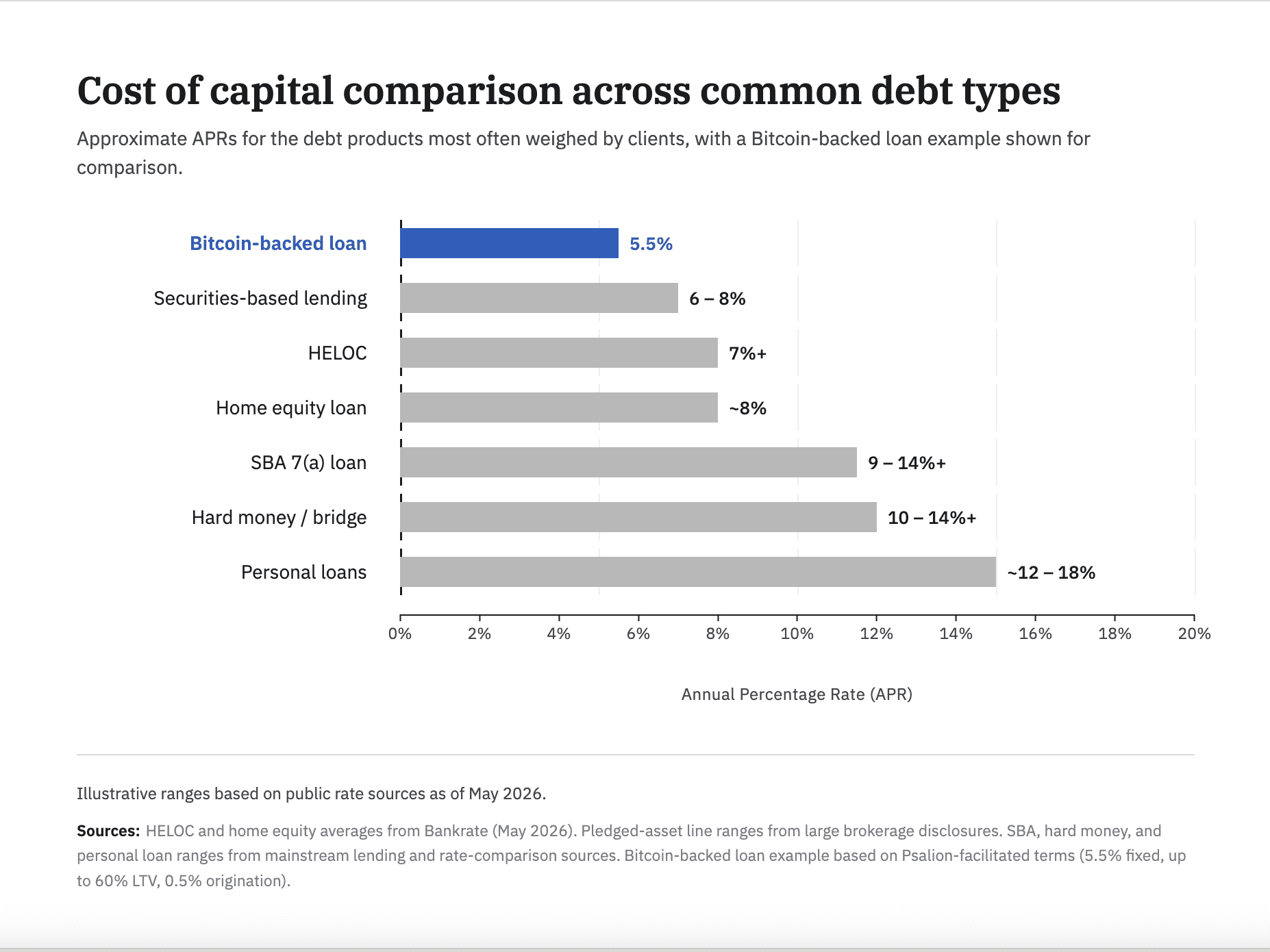

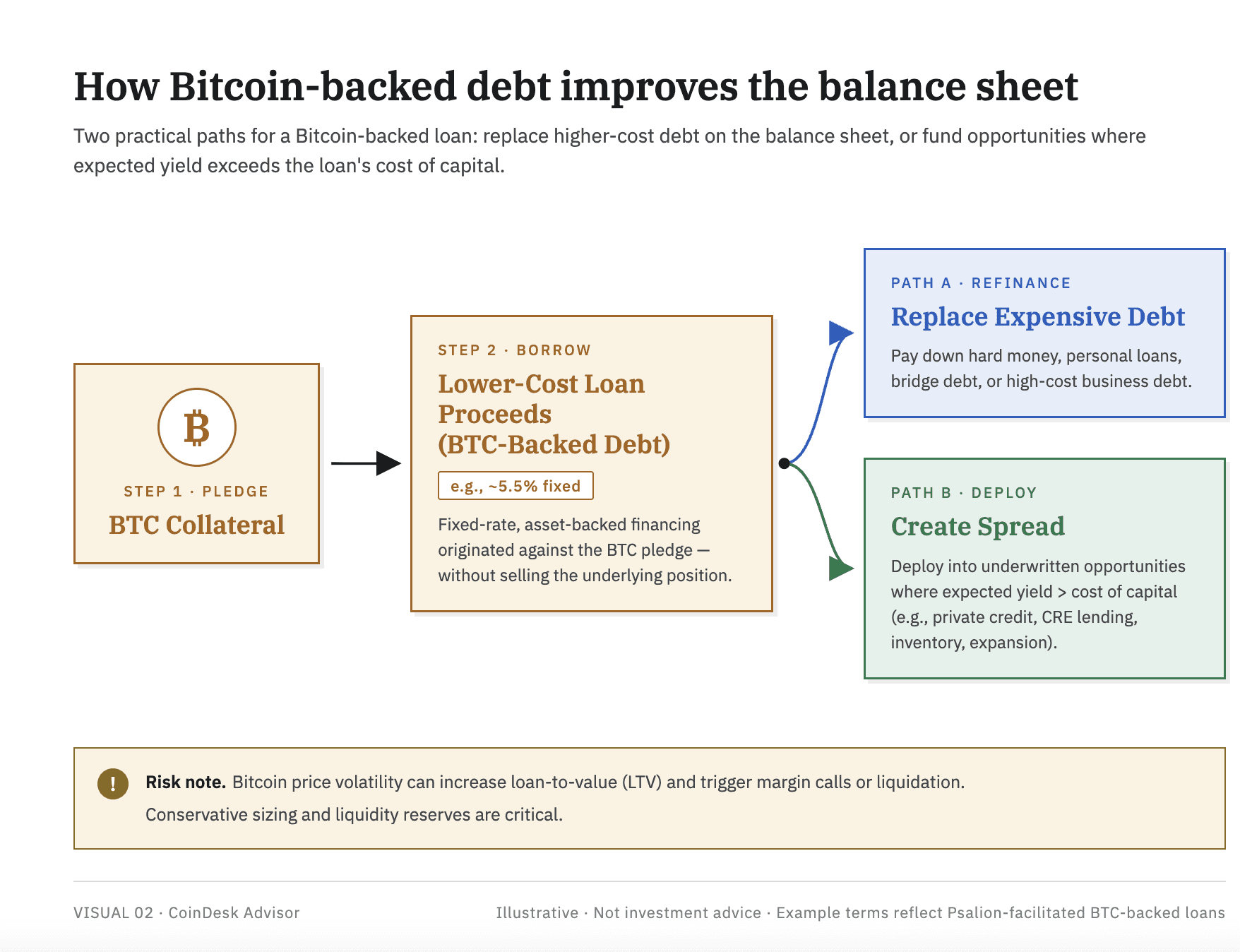

Bitcoin-backed lending is being repositioned inside institutional advisory workflows as a cost-of-capital question rather than a crypto trade, according to this week's Crypto Long & Short newsletter from CoinDesk. Alec Beckman, VP of the Americas at Psalion, argues that debt-heavy professionals — real estate investors, founders, advisors and small-business owners — should benchmark BTC-collateralised credit against HELOCs above 7%, securities-based lending at 6–8%, hard-money and bridge loans at 10–14% plus points, and personal loans in the low-to-mid teens. Psalion's own structure — a 5.5% fixed rate, up to 60% LTV, 0.5% origination fee — is offered as one data point in that comparison.

Why it matters

The reframe matters because it changes who the relevant buyer is. The pitch is no longer aimed at crypto-native traders hedging exposure or chasing leverage; it is aimed at incumbent borrowers who already own BTC and already carry conventional debt. Beckman frames three decision levers — rate, fees and friction — and argues that collateral-first underwriting lets lenders skip income verification, tax returns, appraisals, personal guarantees and covenants, producing faster access to dollars or stablecoins against a verifiable, continuously monitored asset. The collateral-risk caveats are explicit: BTC volatility can breach LTV thresholds, trigger margin calls and create taxable liquidation events, so the product is sized for clients who understand the asset, not sold as a universal upgrade.

Market impact

The newsletter pairs that reframing with a parallel argument from Serena Sebastiani, chief strategy officer at Fuze, that stablecoins are no longer a crypto product but settlement infrastructure for the world's most under-served payment corridors. She cites live stablecoin rails operating under 1% in Gulf-to-South-Asia, intra-African and CIS-to-MENA flows versus an 8.3% average cost for Sub-Saharan remittances — roughly triple the UN's 3% SDG target — and notes the $136 billion African SME trade finance gap and a $3.4 trillion AfCFTA market where Chinese traders are already settling in USDT. The week's headlines reinforce the institutional plumbing: the Clarity Act cleared a Senate committee 15-9, JPMorgan filed a tokenised JLTXX fund on Kinexys structured to GENIUS Act reserve rules, BlackRock's $2.2B BUIDL and Janus Henderson's $1.1B JTRSY gained instant-redemption access via Grove's $1B Basin facility, Galaxy won a New York BitLicense on a $9B prime platform, and Solana's tokenised RWA market cap jumped 43% QoQ to $2.01B.

Frequently asked questions

-

What rate does Bitcoin-backed lending actually carry today?

Psalion's structure cited in the newsletter is 5.5% fixed, up to 60% LTV, with a 0.5% origination fee. Market rates vary widely, but that data point undercuts HELOCs above 7%, securities-based lending at 6–8% and hard-money or bridge loans at 10–14% plus points.

-

Who is the target borrower for BTC-collateralised credit?

Debt-heavy professionals who already own Bitcoin — real estate investors, founders, small-business owners and advisors with clients carrying conventional debt — not crypto-native traders chasing leverage. The pitch is to benchmark BTC collateral against the borrower's existing debt stack, not to allocate fresh BTC…

-

Why are stablecoins being framed as settlement infrastructure?

Live stablecoin rails in Gulf-to-South Asia, intra-African and CIS-to-MENA corridors operate at under 1%, versus an 8.3% average cost for Sub-Saharan remittances — nearly triple the UN's 3% SDG target. Regulators in the UAE, Rwanda, Kazakhstan and the Philippines are now designing frameworks specifically for that…

-

What are the main risks of borrowing against Bitcoin?

BTC volatility can push LTV past agreed thresholds and trigger margin calls or forced liquidation, which itself can create a taxable event. The newsletter explicitly sizes the product for borrowers who understand the asset and maintain liquidity buffers below maximum LTV.

-

Which institutional milestones did the newsletter flag this week?

The Clarity Act cleared a US Senate committee 15-9, JPMorgan filed the tokenised JLTXX fund on Kinexys to GENIUS Act reserve standards, BlackRock's $2.2B BUIDL and Janus Henderson's $1.1B JTRSY gained instant redemptions via Grove's $1B Basin facility, Galaxy won a New York BitLicense on a $9B prime platform, and…