CoinDesk

CoinDesk

The U.S. Senate Banking Committee has advanced the Digital Asset CLARITY Act, a bipartisan compromise brokered by Senators Thom Tillis (R-NC) and Angela Alsobrooks (D-MD) that explicitly prevents fintech platforms from treating stablecoins as interest-bearing accounts while still letting them pay rewards and bonuses the way banks and credit card issuers do. Banking lobby groups are now pushing to strip even those rewards, threatening to derail the bill before a full Senate vote. With 88% of global crypto trading volume already sitting on non-U.S. exchanges and foreign-issued stablecoins handling roughly 75% of stablecoin volume, the stakes for U.S. consumer finance and capital-markets leadership are concrete — not rhetorical.

Why it matters

Alex Tapscott, CEO of CMCC Global Capital Markets, argues the average American consumer is being lost in the political horse-trading. Americans paid about $5.8 billion in overdraft fees in 2023 according to the CFPB, with nearly 80% of those charges concentrated in just 9% of accounts, while the average savings rate sits at 0.38%. The Crypto Council for Innovation puts U.S. crypto ownership at roughly one in five adults — about 68.5 million people — and four in five merchants believe accepting crypto could help attract new customers. Under the GENIUS and CLARITY frameworks, stablecoin issuers would have to meet reserve, transparency, AML, cybersecurity and consumer-protection requirements, giving regulators a perimeter to police inside rather than offshore.

Market impact

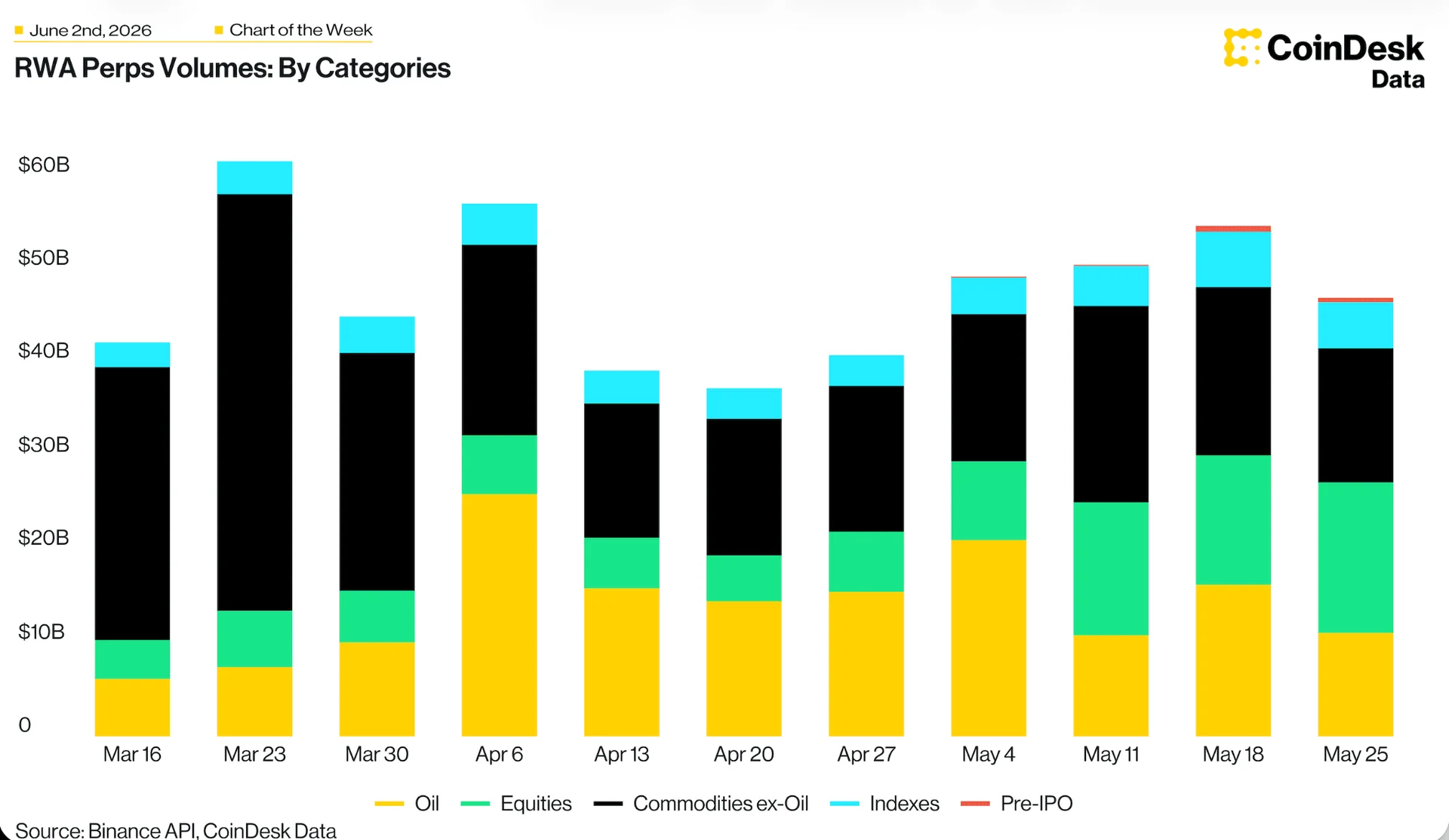

Aisha Hunt, founder of Kelley Hunt PLLC, frames the next leg of growth as upgrading Wall Street wrappers rather than replacing them. F/m Investments and The RBB Fund filed what is believed to be the first exemptive application on January 21, 2026, seeking SEC permission to tokenize shares of TBIL, the U.S. Treasury 3 Month Bill ETF, on a permissioned ledger. Citi projects tokenized securities could scale to a $5.5 trillion market by 2030, including up to $1 trillion in onchain U.S. T-bill demand and $2.6 trillion in tokenized stocks. On the venue side, RWA perp volume runs $45–60 billion a week and is rotating from commodities into equities, which have roughly tripled to about $18 billion — a sign that crypto-venue derivatives are increasingly used for 24/7 equity exposure. If CLARITY stalls and yield-bearing stablecoin rewards are gutted, that tokenization pipeline migrates offshore; if it passes, U.S. issuers get the regulatory perimeter to compete for it.

Frequently asked questions

-

What is the CLARITY Act and where does it stand?

The Digital Asset Market CLARITY Act is legislation that would set clear rules for digital assets in the U.S. The Senate Banking Committee recently advanced the bill after a bipartisan compromise brokered by Senators Tillis and Alsobrooks, but banking lobby groups are still pushing to weaken it before a full Senate…

-

Why are banks fighting stablecoin rewards?

Banks want to block fintech platforms from paying rewards on stablecoins that resemble bank deposit economics. The current CLARITY compromise already bars fintechs from treating stablecoins as interest-bearing accounts, but permits rewards and bonuses — and bank groups are pushing to strip even those.

-

How many Americans already own crypto?

According to the Crypto Council for Innovation, roughly one in five American adults — about 68.5 million people — now own cryptocurrency, with stablecoins especially popular among younger consumers, immigrants, freelancers and underserved communities.

-

What is the tokenized ETF application F/m Investments and RBB Fund filed?

On January 21, 2026, F/m Investments LLC and The RBB Fund, Inc. filed what is believed to be the first exemptive application by an ETF issuer seeking to tokenize shares of an exchange-traded fund — TBIL, the U.S. Treasury 3 Month Bill ETF — on a permissioned blockchain ledger. The application is pending before the SEC.

-

How big could the tokenized securities market get?

Citi projects tokenized securities could grow into a $5.5 trillion market by 2030, driven by up to $1 trillion in onchain U.S. Treasury bill demand and $2.6 trillion in tokenized stocks.