CoinDesk

CoinDesk

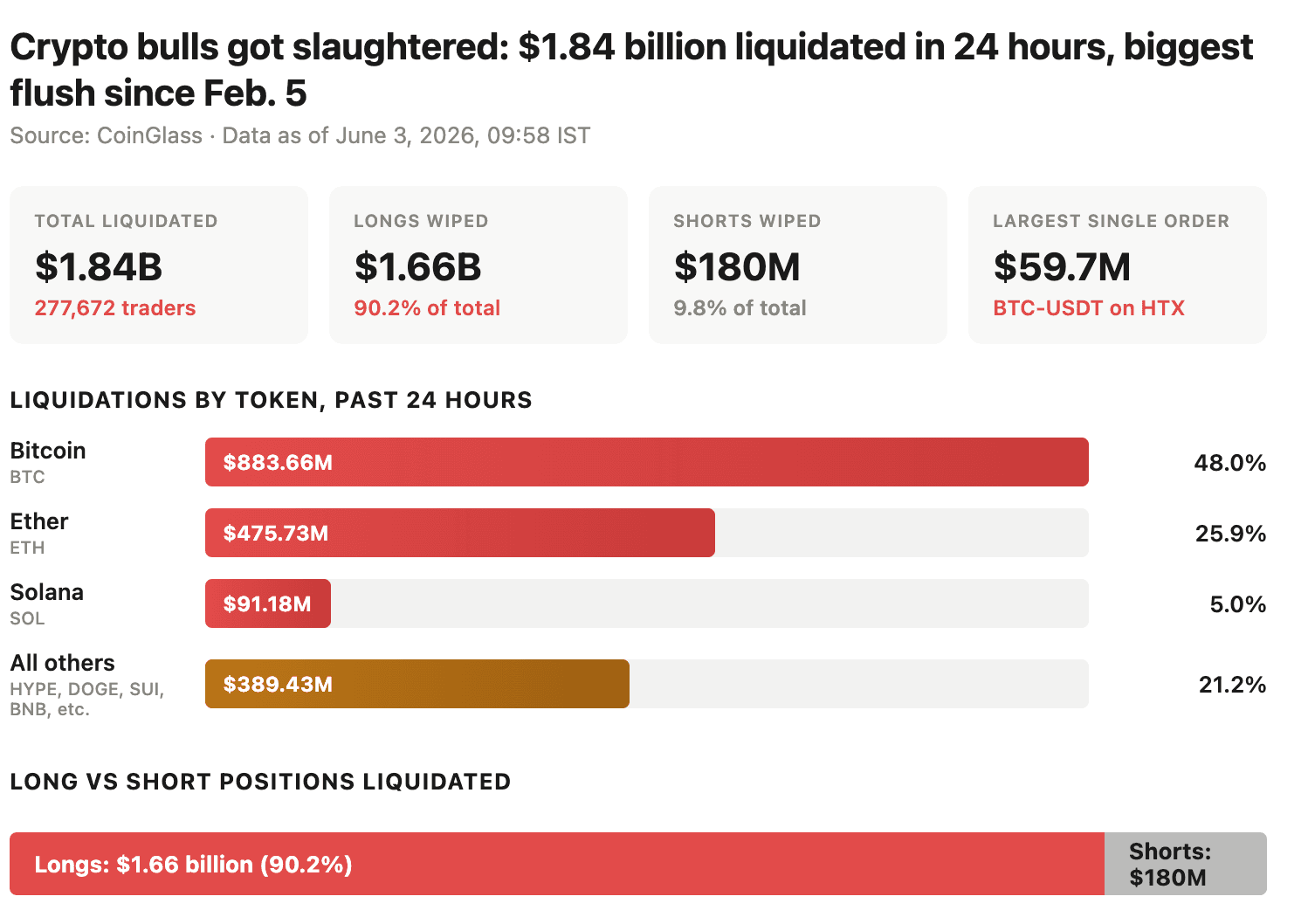

Roughly $1.84 billion in leveraged crypto positions were forcibly closed in 24 hours, with $1.66 billion of that coming from long bets, the largest wipeout since February 5. Bitcoin fell 6.4% to a 24-hour low of $65,708 and ether broke below $1,900 in Asian trading, even as the MSCI All Country World Index set a fresh all-time high on the AI rally. Solana and DOGE each dropped about 9%, with the single largest order a $59.67 million BTC-USDT long unwound on HTX.

Why it matters

The cascade landed in a market that had been pricing a catch-up trade to global equities, and it landed hard. Major cryptos tumbled as stock indexes hit records, with bitcoin down as much as 12.3% on the week and ether off 11.1%. The selling followed MicroStrategy's first disclosed bitcoin sale, spot BTC ETF outflows exceeding $3.2 billion, and a broader unwind of leverage that had been quietly rebuilding into the rally. The divergence between crypto and risk assets is the story — this wasn't a macro deleveraging, it was a crypto-specific flush.

Market impact

Binance absorbed $748 million of the liquidations, roughly 41% of the cascade, with Hyperliquid and Bybit handling $314 million and $247 million respectively. The positioning underneath is uneven: retail traders on Binance, OKX, and Bybit are still leaning long at ratios of 2.22, 2.01, and 1.58, refusing to capitulate. Whale accounts on OKX have flipped to a 0.54 long-short ratio, flagged as extremely bearish. Open interest climbed from roughly 759,000 BTC to 788,600 BTC even as the long book was being wiped out — a sign fresh shorts are building on top of the flush rather than the cascade finding a clearing level. A break below $65,000 opens a path toward $60,000; a hold could allow a relief bounce, though the positioning data argues against the bounce being the base case.

Frequently asked questions

-

How much was liquidated in the crypto market in this event?

Roughly $1.84 billion in leveraged crypto positions were forcibly closed in 24 hours, with $1.66 billion coming from long bets. It was the largest liquidation cascade since February 5.

-

Why is rising open interest during a price drop a bearish signal?

When open interest climbs while price falls, it typically means new short positions are opening on top of longs being closed. The cascade has not found a clearing level and fresh bearish bets are still being built.

-

How did the major exchanges split the liquidation volume?

Binance absorbed about $748 million, or roughly 41% of the cascade. Hyperliquid handled $314 million and Bybit logged $247 million, with the vast majority of liquidated positions on each venue being longs.

-

Why did crypto fall while global stock indexes hit records?

The sell-off was crypto-specific rather than a broad macro deleveraging. It followed MicroStrategy's first disclosed bitcoin sale, spot BTC ETF outflows exceeding $3.2 billion, and the unwind of leverage that had quietly rebuilt into the rally.

-

What price levels are traders watching next?

A break below $65,000 on bitcoin opens a path toward $60,000, while a hold could allow a relief bounce. The positioning data — retail still long, whales flipped short, OI still rising — argues against the bounce being the base case.