CryptoSlate

CryptoSlate

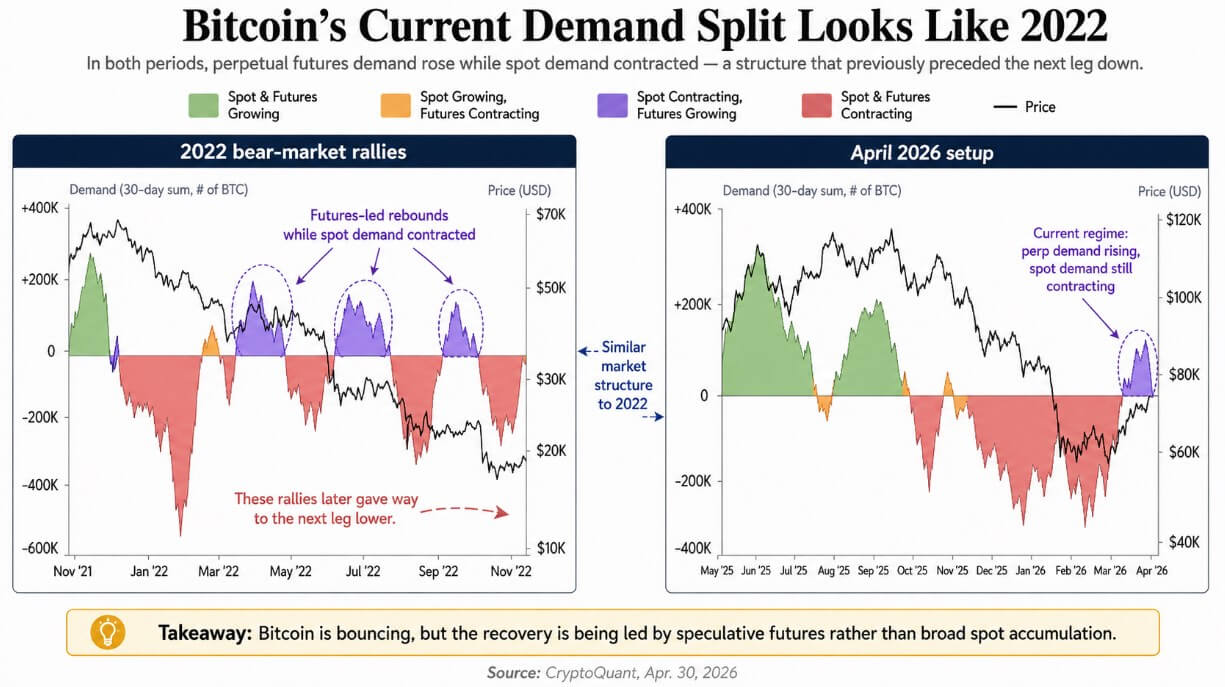

CryptoQuant's Apr. 30 read shows Bitcoin's recovery is being financed almost entirely by perpetual futures, not spot demand — the same market structure that defined the failed bear-market rallies of 2022, when leverage-driven bounces resolved into the next leg lower.

CoinGlass data captures the split: $47.64 billion in 24-hour Bitcoin futures volume against $4.07 billion in spot, an 11.7x ratio, with open interest near $54.19 billion as of Apr. 30. Some platforms extend leverage to 50x collateral, which means a relatively small adverse move can force a large unwind into a $4-billion-a-day spot book.

Why it matters

The 2022 parallel is structural, not cosmetic. In each of that year's bear rallies, perpetual futures demand recovered first while spot contracts contracted — leveraged traders financed the bounce, then came off as cash buyers proved too thin to absorb the selling. Bitcoin's current April 2026 move sits in that regime, with borrowed capital reappearing before real demand does.

The scale is now bigger. A $54 billion open-interest base sitting against $4 billion of daily spot volume is a depth problem that didn't exist at the same magnitude in 2022. Farside Investors data shows aggregate US spot Bitcoin ETF outflows of $490.5 million between Apr. 27 and Apr. 29 — the ETF bid has gone choppy at exactly the moment futures positioning is expanding.

Market impact

The bull trigger is CryptoQuant's apparent-demand measure moving back above zero before open interest unwinds — spot accumulation confirming the futures-led move. That hasn't happened yet. The bear case needs only leveraged traders to reduce exposure before spot demand turns positive, and a partial unwind at $54 billion in open interest produces large absolute selling into a thin spot book.

The structural gap from 2022 does give longs a foundation: US spot Bitcoin ETFs now hold roughly $58.1 billion cumulative, with IBIT alone near $65.2 billion, and IBIT absorbed about $1.47 billion in net inflows between Apr. 13 and Apr. 29. That institutional bid didn't exist four years ago.

Frequently asked questions

-

What is the futures-to-spot volume ratio telling us about Bitcoin's rally?

CoinGlass data shows $47.64 billion in 24-hour Bitcoin futures volume against $4.07 billion in spot as of Apr. 30 — an 11.7x ratio. CryptoQuant reads this as leverage driving the move rather than committed cash demand, the same split that defined 2022's failed bear rallies.

-

Why are analysts comparing Bitcoin's April 2026 setup to 2022?

CryptoQuant's Apr. 30 note flags perpetual futures demand recovering while spot contracts contract — the regime that produced 2022's bear rallies, where leveraged bounces resolved into the next leg lower because cash buyers were too thin to absorb selling.

-

How big is the open-interest risk if leveraged longs unwind?

Bitcoin open interest sat near $54.19 billion as of Apr. 30. Some platforms extend leverage to 50x collateral, so a partial unwind against roughly $4 billion in daily spot volume is a depth problem — liquidations can press prices lower before spot demand deepens enough to hold a floor.

-

What do US spot Bitcoin ETF flows look like right now?

Farside Investors data shows aggregate US spot Bitcoin ETF outflows of $490.5 million between Apr. 27 and Apr. 29. The near-term ETF bid has turned choppy, though longer-term the category holds roughly $58.1 billion cumulative and IBIT alone is near $65.2 billion.

-

What would invalidate the 2022-style bear case for Bitcoin?

CryptoQuant's apparent-demand measure moving back above zero before open interest unwinds — spot accumulation confirming the futures-led move. The structural offset is real: regulated US spot ETFs, deeper institutional infrastructure, and a corporate-treasury bid that did not exist in 2022.