CryptoSlate

CryptoSlate

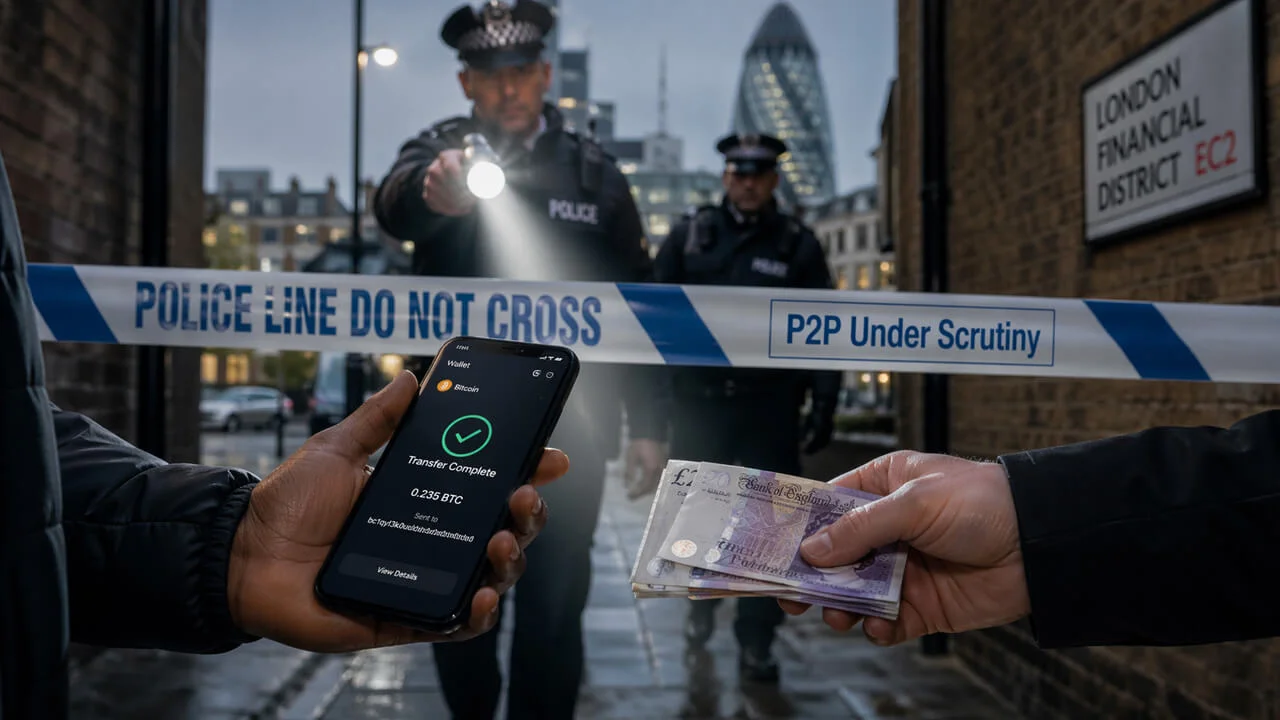

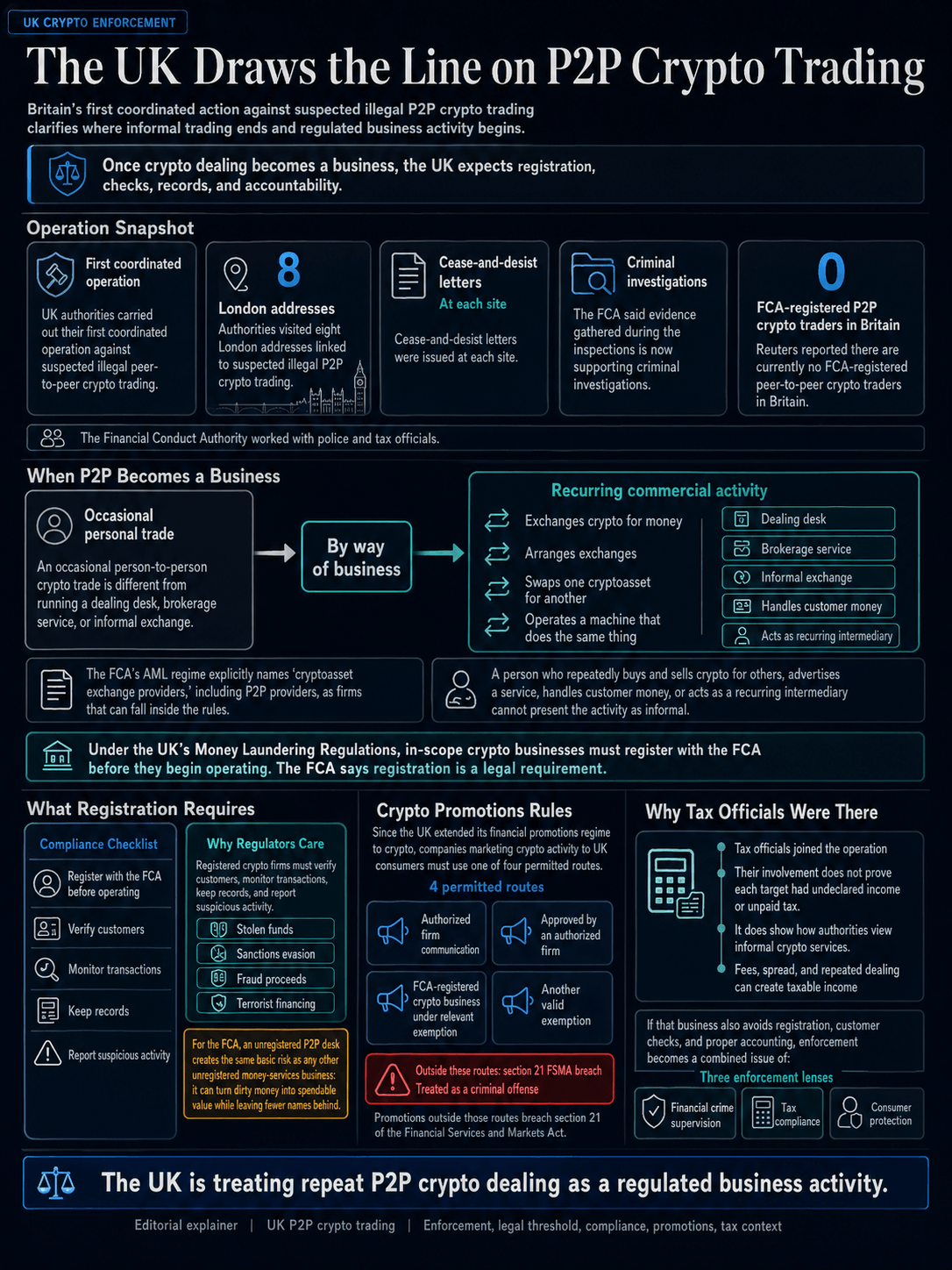

UK authorities carried out their first coordinated operation against suspected illegal peer-to-peer crypto trading this week, with the Financial Conduct Authority joining police and HMRC tax officials in visiting eight London addresses. Cease-and-desist letters were issued at each site, and evidence gathered during the inspections is now supporting criminal investigations. Reuters reported that there are currently no FCA-registered peer-to-peer crypto traders in Britain — meaning any repeat dealing activity sits outside the regulator's perimeter.

Why it matters

The legal line is well-defined even if the enforcement is new. Under the UK's Money Laundering Regulations, in-scope crypto businesses — including peer-to-peer providers, cryptoasset exchange providers, and crypto ATM operators — must register with the FCA before they begin operating. A person who regularly exchanges crypto for money, arranges those exchanges, swaps one cryptoasset for another, or operates a machine that does the same "by way of business" is treated as a financial-services firm, not an occasional trader. The FCA's anti-money-laundering regime explicitly names peer-to-peer providers as firms that can fall inside the rules.

Having tax officials in the room widens the exposure. A business that takes fees, earns spread, or generates gains through repeated dealing can create taxable income. When that business also avoids registration, customer checks, and clean accounting, enforcement collapses the usual silos — financial-crime supervision, tax compliance, and consumer protection wrap into a single operation. Section 21 of FSMA adds another layer: marketing crypto to UK consumers outside one of four permitted routes is a criminal offence in its own right.

Market impact

For registered exchanges, custodians, and banks eyeing compliant crypto rails, the raid is legitimising — informal counterparties that once sat beside them on the margin are being pushed off it. For users who relied on informal access — the unbanked, cross-border workers, people without standard documents, or anyone deliberately avoiding monitored rails — the squeeze funnels activity toward platforms that can be pressured, licensed, delisted, acquired, or cut off from banking. Privacy, access, and autonomy all narrow in the same direction.

Frequently asked questions

-

What did the FCA actually do in London this week?

The FCA joined police and HMRC tax officials in visiting eight London addresses linked to suspected illegal peer-to-peer crypto trading. Cease-and-desist letters were issued at each site, and evidence gathered is now supporting criminal investigations.

-

How many FCA-registered peer-to-peer crypto traders are there in the UK?

According to Reuters reporting, there are currently no FCA-registered peer-to-peer crypto traders in Britain — meaning repeat dealing activity sits outside the regulator's perimeter.

-

What makes someone an unregistered crypto business under UK law?

Under the Money Laundering Regulations, a person who regularly exchanges crypto for money, arranges those exchanges, swaps one cryptoasset for another, or operates a machine doing the same "by way of business" is treated as a cryptoasset exchange provider — and must register with the FCA before operating.

-

Why is HMRC involved in an FCA enforcement action?

A business that earns fees, spread, or gains from repeat dealing can create taxable income. When that business also avoids registration, customer checks, and clean accounting, financial-crime supervision, tax compliance, and consumer protection collapse into a single investigation.

-

How does this fit the broader UK crypto regulatory timeline?

The raid is part of a longer UK push to pull crypto from a semi-detached market into a rule-bound financial box, with the Treasury's October 2027 deadline for a full FSMA-style cryptoasset regime as the next scheduled milestone.