WuBlockchain

WuBlockchain

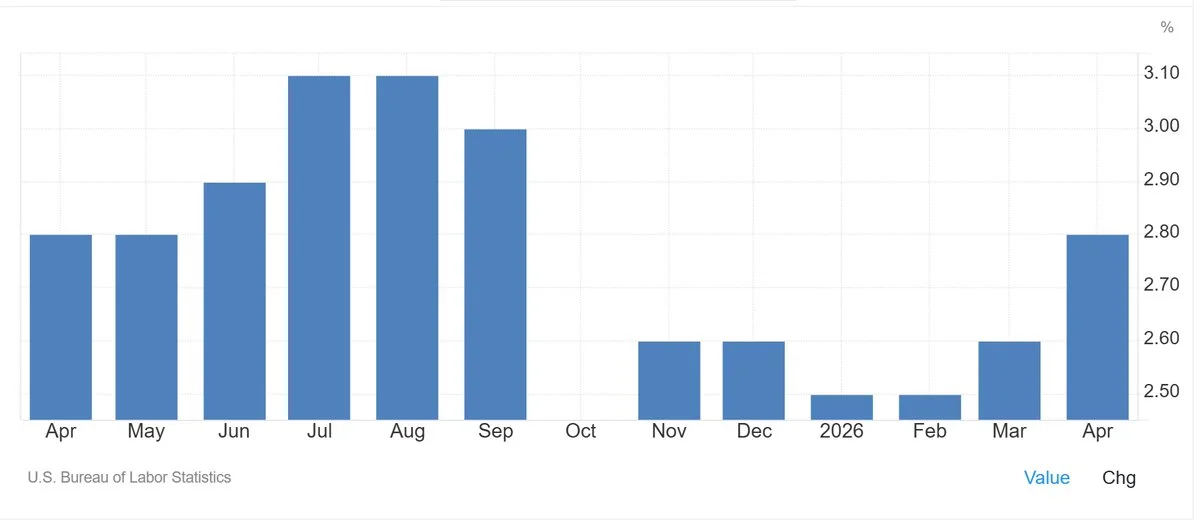

April's U.S. CPI print came in hotter than expected on every key measure. Headline CPI rose 3.8% year over year, above the 3.7% consensus, while core CPI climbed 2.8% YoY versus the 2.7% estimate. On a monthly basis, core CPI rose 0.4% seasonally adjusted, also above the 0.3% estimate.

Why it matters

Core inflation is now at its highest annual pace in seven months, undoing the disinflation narrative the Fed has been building toward since late last year. Services excluding energy services rose 3.3% YoY, with shelter up 3.3% and transportation services up 4.3% — the stickier, wage-driven components of the basket that the Fed explicitly watches when deciding on rate cuts.

Market impact

The print crushed rate-cut expectations: futures markets quickly repriced the timing and total size of 2026 Fed easing, and risk-off flows hit equities while the dollar strengthened. Sticky services inflation is the exact signal that pushes the Fed's reaction function toward a higher-for-longer stance — bad for duration, bad for risk assets priced on cheap-money assumptions, and a structural headwind for crypto multiples funded by leveraged rate-cut bets. Watch the next two CPI prints: any follow-on heat locks in the repricing; a cool print opens a relief window.

Source: [United States Core Inflation Rate](https://tradingeconomics.com/united-states/core-inflation-rate)

Frequently asked questions

-

What did the April U.S. CPI report show?

Headline CPI rose 3.8% year over year and core CPI 2.8% YoY — both above consensus. Core CPI also rose 0.4% month over month on a seasonally adjusted basis versus the 0.3% estimate, marking a 7-month high in annual core inflation.

-

Which CPI components drove the hot print?

Services excluding energy services rose 3.3% year over year, led by shelter (+3.3%) and transportation services (+4.3%). Apparel prices rose 4.2% YoY, new vehicles edged up 0.2%, while used cars and trucks fell 2.7%.

-

How did markets react to the April CPI surprise?

Futures markets quickly repriced the size and timing of expected 2026 Fed rate cuts, with risk-off flows hitting equities and the dollar strengthening. Higher-for-longer returned as the working assumption for Fed policy.

-

Why does the Fed focus on core CPI rather than headline?

Core CPI strips out volatile food and energy prices to expose the underlying inflation trend. Services inflation, which is wage-driven, is considered sticky and central to the Fed's reaction function on rate cuts.

-

What would invalidate the higher-for-longer repricing?

A cooler follow-on CPI print in the next two releases would reopen a relief window. Continued heat across services and shelter would lock in the repricing and reinforce the Fed's restrictive stance into late 2026.