CryptoSlate

CryptoSlate

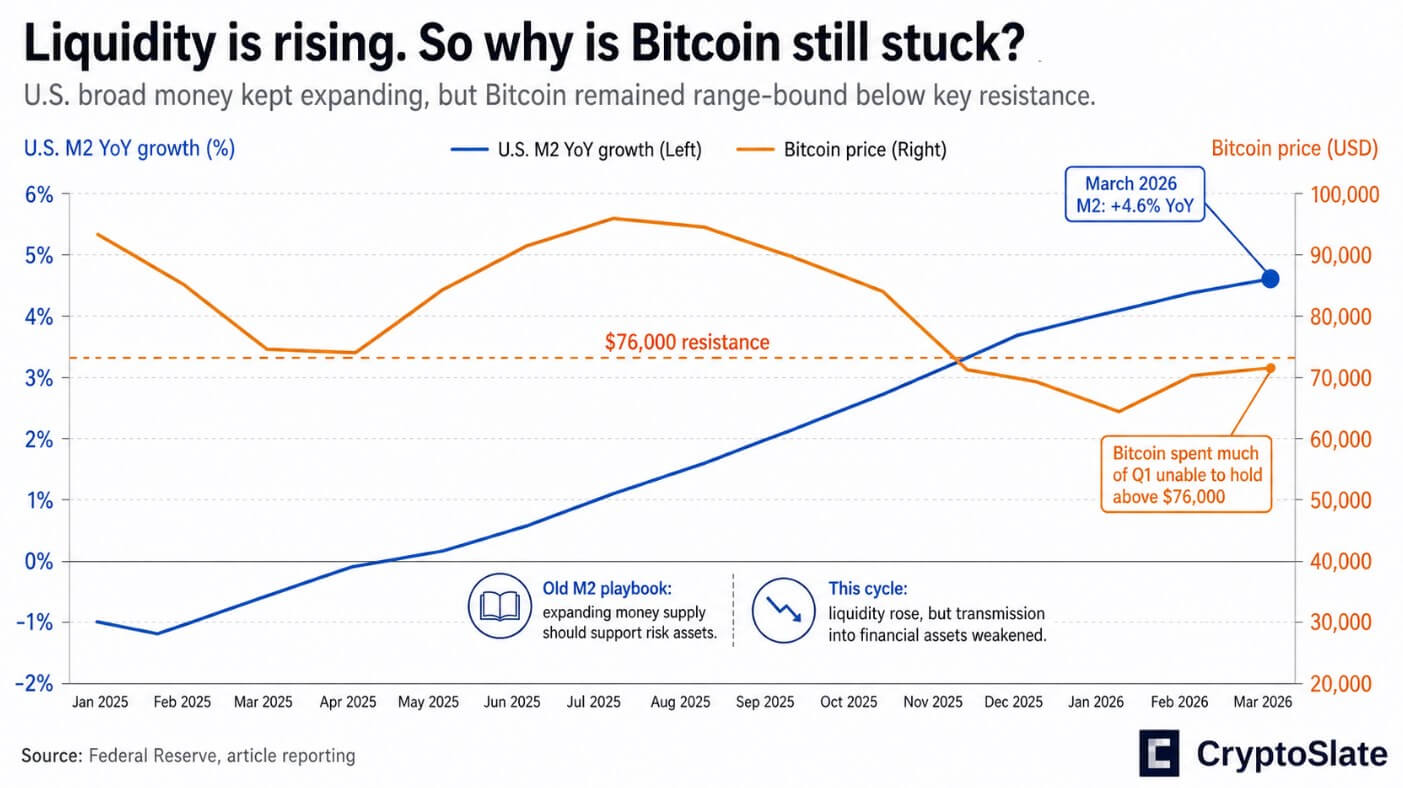

Bitcoin has spent the first quarter of 2026 unable to hold above $76,000 despite a global M2 money supply that printed at roughly $22.7 trillion in March, up 4.6% year over year. The old playbook — chart M2 expanding, watch Bitcoin follow — broke when US public debt closed Q4 2025 at over $38.5 trillion, up 6.3% over the same period, leaving debt growth running nearly two percentage points ahead of broad money. The debt-to-M2 ratio now sits at roughly 1.7x, a level with no modern precedent in an environment the market still treats as accommodative.

Why it matters

The transmission mechanism from broad money to risk assets has changed, according to Real Vision chief crypto analyst Jamie Coutts on CryptoQuant's Unbiased podcast. In the post-2008 QE era, the Fed bought assets directly and flooded the system with bank reserves that had nowhere to go but into equities, credit, and eventually crypto. Today, Treasury issuance, reserve management, cash balance swings, and bank credit creation have replaced the balance-sheet firehose — and not all of those channels reach Bitcoin.

The Treasury General Account held roughly $1 trillion in the latest H.4.1 release, draining reserves from the banking system even as M2 ticked up. Reserve balances fell to about $2.9 trillion in the Fed's April 22 release, down roughly $355 billion from a year earlier. The April 29 FOMC held the policy rate at 3.5%-3.75% with total assets around $6.7 trillion, no balance-sheet expansion on the agenda, and inflation cited as the primary restraint. Broad money expands on paper while the plumbing that actually moves reserves into financial markets tightens at the margin.

Market impact

Gold confirms the cross-market read: central banks bought 244 tonnes in Q1, up 3% YoY, with total gold demand reaching 1,231 tonnes and a record $193 billion by value per the World Gold Council. Official institutions are hedging sovereign debt credibility at scale, but through gold — an asset central banks can legally hold. The IMF's latest Fiscal Monitor projects global public debt reaching 100% of GDP by 2029, and the CBO sees US debt held by the public expanding from 101% to 120% of GDP by 2036, a structural supply overhang competing with risk assets for the same pool of reserves and capital.

Coutts frames two outcomes. The bull case — inflation cools, the Treasury cash balance declines, reserves rebuild, bank credit keeps expanding without a growth scare — lets Bitcoin re-rate quickly because the debt-to-liquidity mismatch prevents marginal tightening.

Frequently asked questions

-

Why has Bitcoin decoupled from the M2 money supply chart?

The transmission mechanism has changed, according to Real Vision's Jamie Coutts. In the post-2008 QE era, the Fed bought assets directly and flooded the system with bank reserves that flowed into risk assets. Today, Treasury issuance, reserve management, and cash balance swings have replaced the balance-sheet firehose…

-

What is the current debt-to-M2 ratio in the US?

US public debt closed Q4 2025 at over $38.5 trillion while global M2 reached roughly $22.7 trillion in March 2026, putting the ratio at approximately 1.7x. That level has no modern precedent in a monetary environment the market still treats as accommodative.

-

How fast are US debt and M2 growing year over year?

US public debt grew 6.3% year over year through Q4 2025, while global M2 grew 4.6% year over year by March 2026. Debt growth is running roughly two percentage points ahead of broad money, which is the gap draining reserves out of the financial system.

-

Where is Jamie Coutts placing Bitcoin's value floor?

Coutts treats the $60,000 zone as a value floor and puts the odds the cycle low is already in at better than 50-50. That call sits inside his bull case: inflation cools, Treasury cash balances decline, reserves rebuild, and Bitcoin re-rates as the liquidity thesis regains traction.

-

What is the bear case for Bitcoin in this debt-versus-liquidity regime?

Debt issuance stays heavy, inflation stays sticky, the Fed cannot ease without reigniting it, and Bitcoin trades as a high-beta risk asset exposed to rates, funding conditions, and periodic deleveraging. The April flash PMI from S&P Global already described growth running close to a 1% annualized pace, suggesting the…