CoinDesk

CoinDesk

Infrastructure is the prevailing currency in digital assets, regardless of which token ultimately facilitates the transaction, Nonco CTO Caue Teixeira argued in the latest edition of CoinDesk's Crypto Long & Short newsletter. The thesis: exchanges, custodians, market makers, and settlement networks now carry more long-term value than any single coin, especially as stablecoins, tokenized deposits, and other real-world assets flood into the rails.

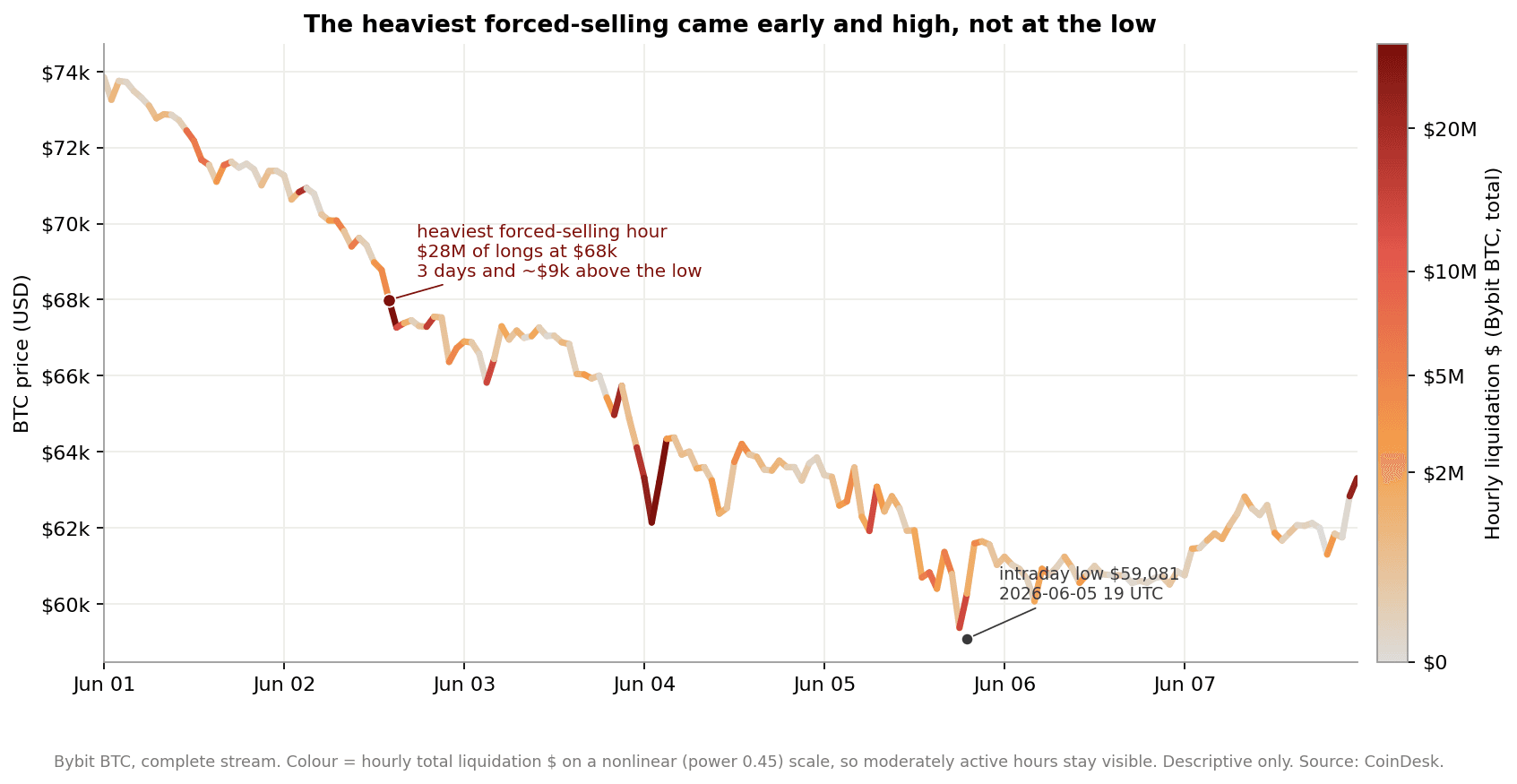

The same issue also features a data-driven look at June's Bitcoin drawdown. Liquibit Capital's Alen Pavlović mapped CoinDesk's liquidation feed onto the price path and found the forced selling peaked early. The heaviest hour of long liquidations, about $28 million, hit on 2 June while BTC still traded near $68,000. The actual bottom, $59,081, did not arrive until 5 June. Leverage cleared while the market was still high; the last leg lower was ordinary spot supply, not blown-out positions.

Why it matters

The two pieces point in the same direction. For institutional allocators, the takeaway is that exposure to the plumbing of crypto, not just the tokens themselves, increasingly defines who captures long-term value. The newsletter's framing fits a year in which RWA perpetual futures volumes hit an all-time high in May even as combined exchange volumes slid 3.45% to $4.41 trillion, the lowest since September 2024.

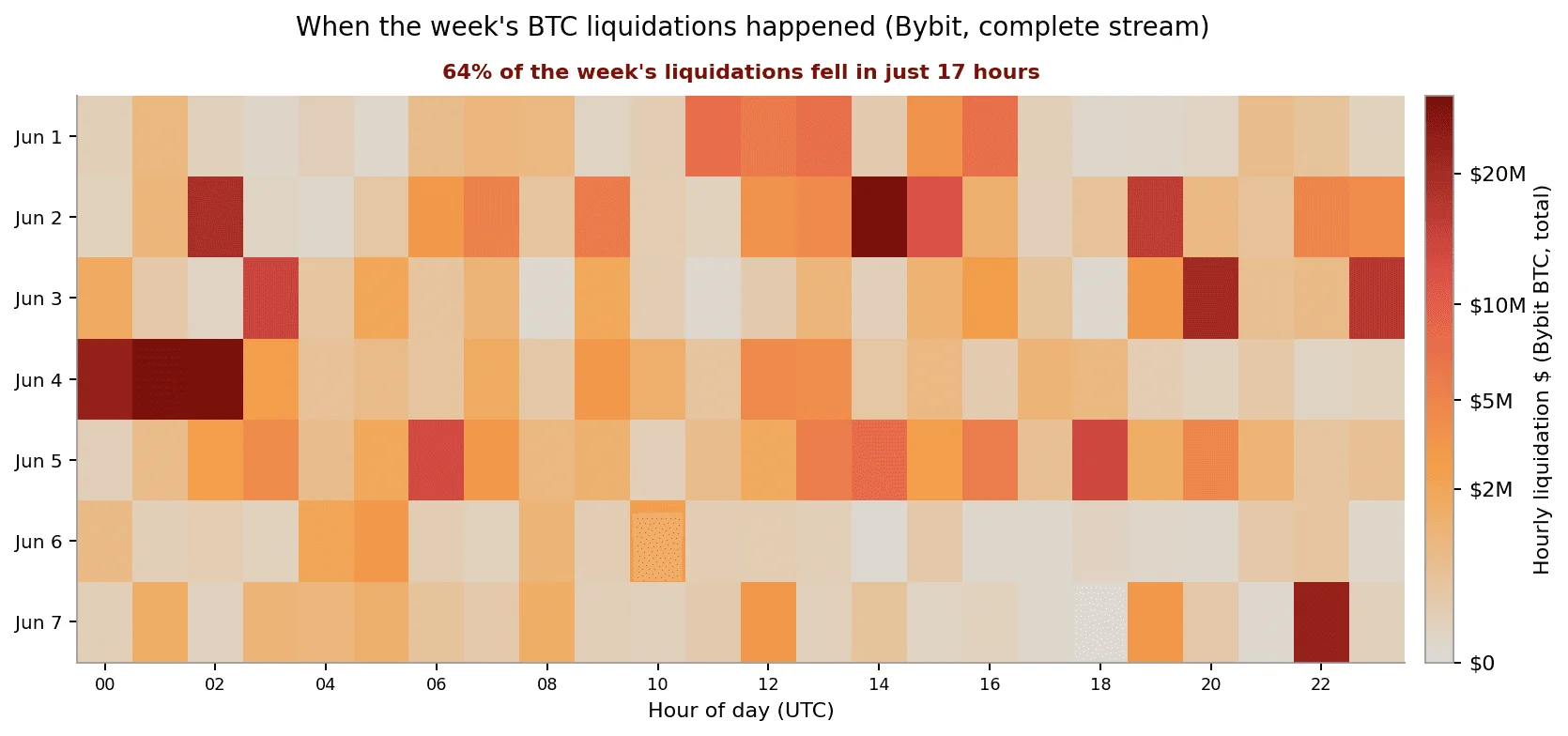

The liquidation timing data is the more actionable read. Pavlović notes that 17 of the week's 168 hours carried 64% of all liquidations, and Bybit's uncapped stream shows roughly $440 million in forced selling, 82% of it longs. Across Bybit, Binance, and OKX, the week cleared at least $1.55 billion. For desks running systematic or basis strategies, the pattern is a reminder that cascade tops tend to print above the eventual price low, not at it.

Market impact

For market structure, the broader point is that the end user is becoming asset-agnostic and infrastructure-dependent. Stablecoins have been the proof case, and tokenized deposits and bonds are now queued behind them. The competitive moat shifts from protocol-level design to operational reliability, custody, compliance, and 24/7 liquidity provision.

The liquidation read also reframes the June $59K bottom. A cascade that clears three days and almost $9,000 above the eventual low is a leverage flush, not a capitulation. Spot, not margin, finished the move, which changes how traders should size the next leg.

Frequently asked questions

-

What is the main argument of this week's Crypto Long & Short?

Nonco CTO Caue Teixeira argues that infrastructure, not any specific coin, is the prevailing currency in digital assets, because exchanges, custodians, and settlement networks carry the long-term value as stablecoins and tokenized real-world assets expand.

-

When did June's Bitcoin liquidation cascade actually peak?

According to Liquibit Capital's analysis of CoinDesk's liquidation feed, the heaviest hour of long liquidations, around $28 million, hit on 2 June while BTC still traded near $68,000, three days and roughly $9,000 above the eventual $59,081 low on 5 June.

-

Why did forced selling stop above the actual bottom?

Leverage was already cleared by 2 June. The final leg from the high $60Ks down to $59,081 was carried by ordinary spot supply rather than blown-out margin positions, which is why the cascade top printed above the price low instead of at it.

-

How concentrated were the June liquidations?

Just 17 of the week's 168 hours carried 64% of all liquidations. Bybit's uncapped stream recorded about $440 million in forced selling, 82% of it longs, and across Bybit, Binance, and OKX the week cleared at least $1.55 billion.

-

What does this mean for the RWA and stablecoin story?

The piece frames end users as increasingly asset-agnostic and infrastructure-dependent. RWA perpetual futures volumes hit an all-time high in May even as combined exchange volumes fell 3.45% to $4.41 trillion, reinforcing that the plumbing, not the token, is where the long-term moat sits.