CoinDesk

CoinDesk

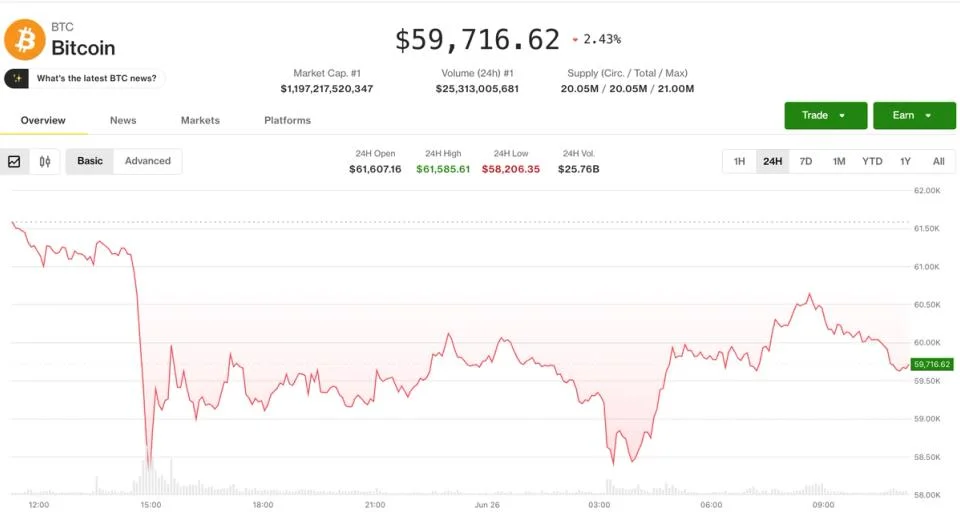

Bitcoin touched $58,100, its weakest level since September 2024, before rebounding to around $59,770. Ether did not follow, sliding another 1% to roughly $1,550 and extending losses to a third straight day, while Nasdaq 100 and S&P 500 futures opened Friday down 1% and 0.4% respectively as the three-month tech rally continued to unwind.

The bounce masked a derivatives market that is clearly leaning defensive. Over $1 billion in leveraged positions, the majority of them longs, were liquidated in 24 hours, and ETH saw more liquidations than BTC over the trailing 12 hours. Bitcoin futures open interest climbed to 778,000 BTC, up sharply from recent lows near 730,000, with the build concentrated during Thursday's late selloff, a pattern consistent with traders adding shorts into weakness rather than covering.

Why it matters

The shape of the open-interest build matters as much as the price action. Rising OI into a falling market means fresh bearish positioning is being put on, not just passive longs being shaken out, which raises the risk of a second-leg flush if support at $58,000 gives way. Ether's open interest has stayed flat near 14 million ETH since mid-June, a more neutral signal that ETH longs are simply capitulating while BTC attracts outright short conviction.

Volatility gauges confirm the shift. Bitcoin's 30-day implied volatility (BVIV) jumped to 53%, its highest since June 7 and up from 39% on June 16. ETH's index climbed to 66%, and on Deribit the one-week BTC options skew is approaching 30%, an unusually steep premium for puts over calls. The VIX at 20% and the Treasury market's MOVE index show equities are not yet in panic mode, but crypto derivatives are pricing in more pain than TradFi is.

Market impact

Flow data backs the bearish read. The OI-adjusted 24-hour cumulative volume delta is negative across most of the top 25 tokens, with only BNB, SOL and TON in the green, and the bias toward market orders over passive limits has held since Tuesday. Block trades added to the picture, including notable demand for the $53,000 BTC put expiring July 10 and ether risk reversals, both one-week bearish hedges from larger accounts.

Frequently asked questions

-

Why is Bitcoin's bounce off $58,000 viewed as fragile?

Bitcoin rebounded to roughly $59,770 after touching $58,100, but derivatives data argues the move is shallow. Futures open interest climbed to 778,000 BTC from recent lows near 730,000 during Thursday's selloff, suggesting traders added shorts into the dip rather than covered, which raises the odds of a second-leg…

-

How much in leveraged positions was liquidated?

Over $1 billion in leveraged crypto positions were liquidated in 24 hours, with longs accounting for the majority. Ether saw more liquidations than Bitcoin over the trailing 12 hours even as BTC absorbed the larger notional open-interest build.

-

What are Deribit options saying about near-term direction?

Deribit's one-week BTC options skew is approaching 30%, a steep premium for puts over calls, and the one- and three-month skews are sending the same message. Block flows added demand for the $53,000 BTC put expiring July 10 and for ether risk reversals, both near-term bearish hedges from larger accounts.

-

How does the crypto volatility spike compare to equities?

Bitcoin's 30-day implied volatility (BVIV) jumped to 53%, the highest since June 7 and up from 39% on June 16. Ether's index climbed to 66%. The VIX at 20% and the Treasury's MOVE index show equities are not in panic mode, but crypto derivatives are pricing in more downside than TradFi volatility gauges.

-

Why is Ethena (ENA) among the worst performers?

ENA fell another 5% on Friday, extending its slide since the June 3 high to 34%. A portion of Ethena's yield strategy depends on positive funding rates, which have now flipped negative, undermining the token's core return mechanism.