What it really is

Crypto arbitrage is the practice of buying an asset where it is cheap and simultaneously selling it where it is expensive, capturing the spread. In theory it is risk-free profit; in practice the costs and competition usually consume the spread before a non-professional can capture it.

Arbitrage exists because markets are not perfectly efficient — different exchanges have different liquidity, different user bases, and different fees. The spreads are usually small, fleeting, and competed away by automation.

How it actually works

Spatial arbitrage

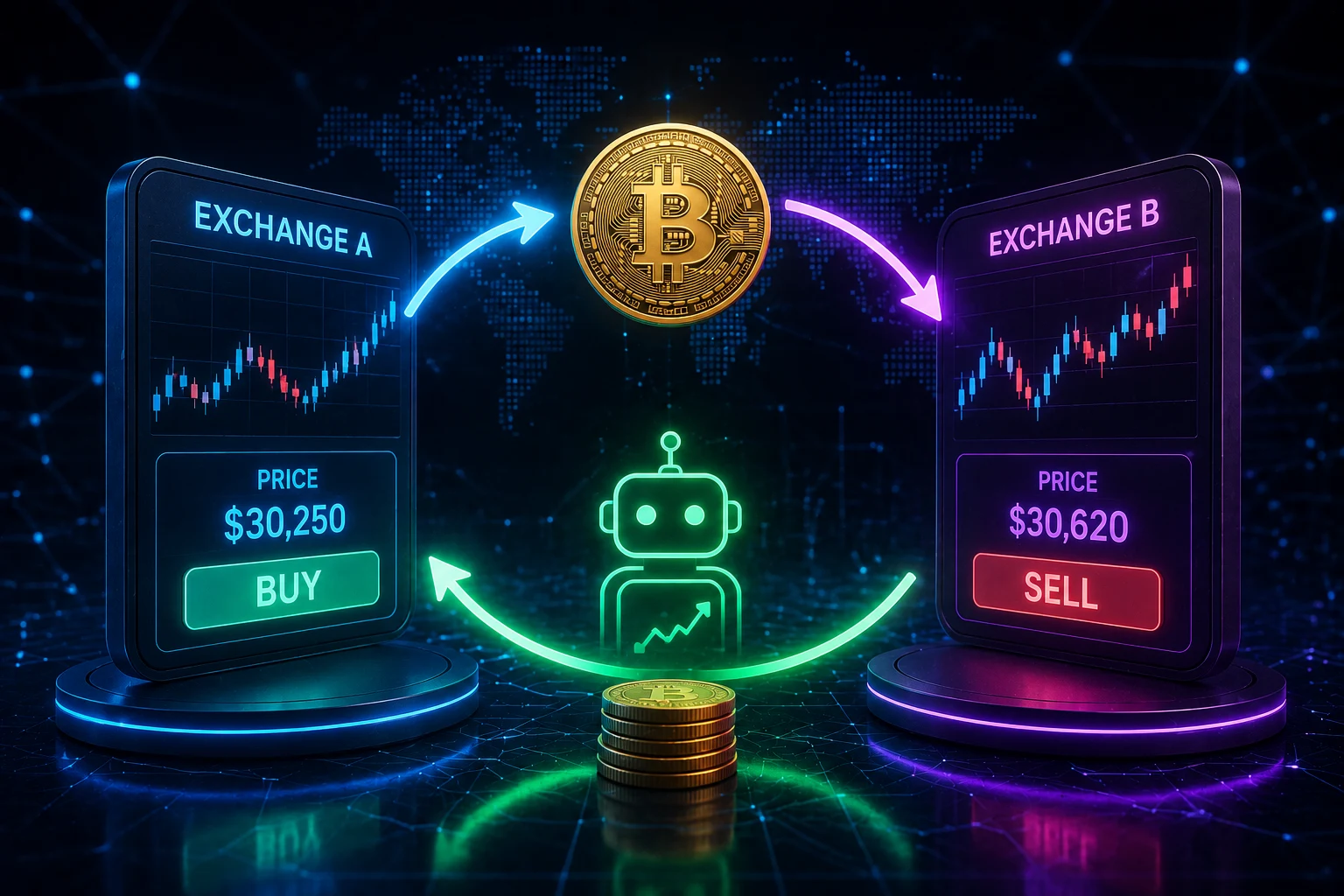

The same asset trades at different prices on two exchanges. You buy on the cheap exchange and sell on the expensive one. In practice you also need pre-positioned inventory on both exchanges (because transferring crypto is too slow to capture short spreads), and the spread has to exceed taker fees on both sides plus risk margin.

Triangular arbitrage

Within one exchange, three trading pairs can be mispriced relative to each other. For example: USD→BTC→ETH→USD should net to ~1.0 after fees; if it nets to 1.005, there is a triangular arbitrage. Bots execute the whole loop in one transaction; humans cannot.

Statistical arbitrage

Correlated assets temporarily diverge from historical relationships. A trader takes opposing positions expecting reversion. This is closer to quantitative trading than pure arbitrage and carries real risk (the relationship may break).

Why most retail arbitrage fails

Fees per leg, slippage in execution, time to transfer assets between exchanges, withdrawal limits, and KYC delays. A spread of 0.5% looks attractive until fees, slippage, and the price moving between your buy and sell turn it into a loss.

A worked example

Spot ETH is $2,000 on Exchange A and $2,015 on Exchange B — a $15 (0.75%) spread. You buy 1 ETH on A: $2,000 + $2 fee = $2,002. You sell 1 ETH on B: $2,015 - $2 fee = $2,013. Gross profit: $11. But you needed ETH pre-loaded on B and USD pre-loaded on A to execute simultaneously; transferring would have taken minutes during which the spread closed. The capital cost (deploying inventory on both exchanges) and operational complexity (rebalancing) consume most of the headline profit. Bots do this thousands of times per day; doing it manually is rarely worth it.

Common mistakes

- Forgetting all fees. Maker, taker, withdrawal, deposit, network — they add up.

- Ignoring transfer time. Crypto transfers can take minutes; spreads close in seconds.

- Underestimating slippage. Large orders move the price in thin books.

- Ignoring exchange counterparty risk. Capital on multiple exchanges multiplies the failure modes.

- Confusing displayed spread with executable spread. Stale quotes, order book depth, and liquidity all matter.

How traders actually do it

Professional arbitrage runs on custom infrastructure: co-located servers, custom exchange APIs, pre-deployed inventory across many exchanges, and risk systems for rebalancing. Retail attempts at simple manual arbitrage usually fail. Some retail-accessible variants — funding rate arbitrage on perpetuals, MEV-resistant DEX flows — exist but require careful study. See technical analysis in crypto for context and crypto risk management for limits.

Spot opportunities in the news context

Major exchange events, regulatory actions, or liquidity shifts sometimes create unusually wide spreads. Zippfeed surfaces crypto headlines with sentiment and importance scoring so you can identify the context behind a wide spread before assuming it is exploitable. None of this is financial advice; it is the context that makes a spread informative rather than just headline-friendly.